Central Bank Digital Currency - A quick overview

Central Bank Digital Currency - A quick overview

Digital money 2 is all about decentralisation. Digital money 2.0 would be a token based digital money. Tokenization is the basis of virtual currencies and that works on blockchain technology. Many countries are in the process of creating their own virtual currencies in the form of Central Bank Digital Currency (CBDC).CBDCs are a liability of the central bank in the same way as physical currency. This is a major differentiator between CBDCs and other tokenized money forms such as cryptocurrencies and stablecoins.

Types of CBDC

I. Wholesale vs retail

Wholesale CBDC- access to CBDC is restricted to limited banks and institutions; Retail CBDC- access is widened to corporates and businesses or generally across the economy to all consumers. The Wholesale system is adopted by developed nations, which have the required infrastructure.

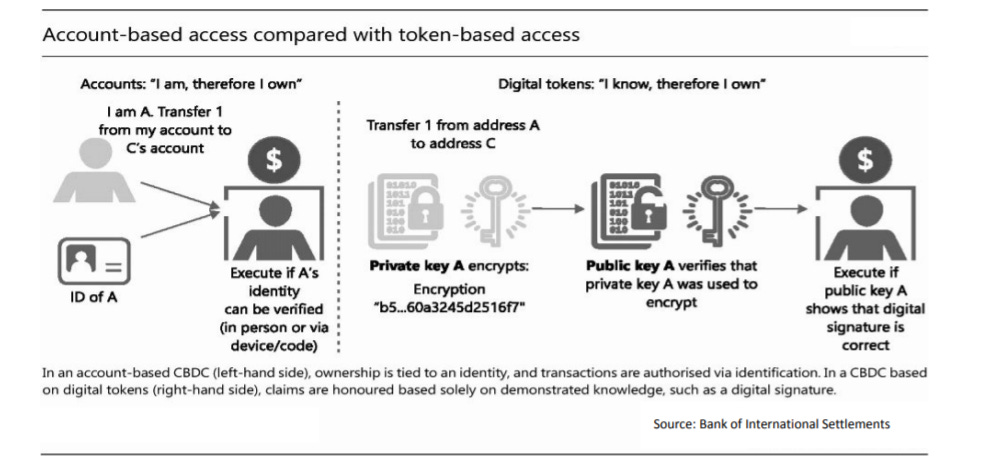

II. Account and Token Based

Account Based CBDC- ownership of the CBDC is aligned to an identity whereby a transaction is an update of payer and payee balance. This is resembling with the current financial or money structure.

Token Based CBDC - in token based CBDC, the token is used with cryptography wherein digital signature is verified by using a public and a private key. Thus, a transaction is a change of ownership of a specific unit of account or token.

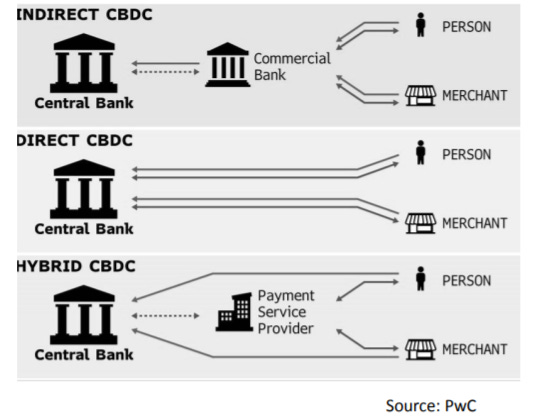

Direct, indirect and Hybrid model

Direct Model: Parties involved in the transaction will hold an account at the central bank. All payment claim will be approved by the central bank. The central bank will work as a permission authority. All KYC compliance shall be done by the central bank.

Indirect Model: The central bank will issue the digital currency token to the commercial bank or fintech company, which will then issue the token or currency and also handle KYC and AML requirements. The responsibility of claim for the currency will be on the commercial bank/fintech company and not on the central bank.

The Hybrid Model: the central bank issues CBDC to a commercial bank or fintech, which handles the transaction and the KYC and AML requirements. However, the responsibility remains with the central bank.

Benefits of CBDC

CBDCs are seen as alternative to the current digital payment system such as banking payment, credit cards etc. The CBDCs can reduce the current cost of managing the cash. CBDC will give more power and authority to central bank, from a regulatory perspective, this would be a more trustworthy step.

Drawbacks of CBDC

As this is a new concept, the countries are planning to implement CBDC also need to work on the drawbacks. There could be a risk if there is too much withdrawal of digital currency, also, there are issues regarding data privacy.

Further, the current legal framework is not enough to address various legal implications of dealing with CBDC. This could pause reputational and legal risks for both users and the banks.